Fraud Is Universal. The Damage Isn’t.

What a National Survey Reveals About Age, Trust, and the Protection

Gap 2,721 bank customers. One striking pattern. And a protection system that isn't reaching the people who need it most.

In my last post, I analyzed 679 reports from the CFPB Consumer Complaint Database, revealing that older Americans are disproportionately harmed by fraud. Just 6.2% of complainants accounted for 37.5% of total losses, averaging $155,379 per case. However, complaint data inherently skews toward the most severe cases; it captures only those motivated enough to file a formal report. This raised a critical question: what about everyone else?

The newly released National Age-Friendly Banking Survey (NAFBS) public use file provides a clearer picture. This rigorously designed, nationally representative survey of 2,721 U.S. adults with bank or credit union accounts features a careful oversampling of adults 60 and older. Over a single weekend afternoon, Over a single weekend afternoon, I leveraged AI tools to build an interactive dashboard, surfacing the realities hidden beneath the summary statistics1.

The Finding That Reframes Everything

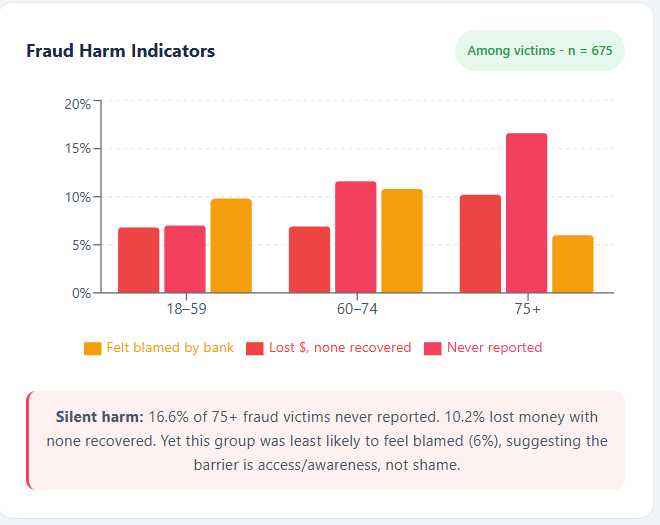

Fraud incidence is nearly identical across all age groups: about 25-27%. Older adults are not targeted more frequently, but the consequences they face are vastly unequal. Among fraud victims aged 75 and older:

10.2% lost money with zero recovery—the highest unrecovered-loss rate of any age group.

16.6% never reported the fraud, more than double the rate of adults aged 18-59 (7%).

3.3% were victimized three or more times in a single year, twice the rate of younger adults.

Notably, this group is the least likely to feel blamed by their bank (6%, compared to 10% for younger adults). This suggests the primary barrier to reporting is not shame, but a lack of access, awareness, or easy-to-use digital tools.

Figure 1. Fraud loss rate, non-reporting rate, and repeat victimization by the age groups.

The Institution People Trust Most

When asked who they’d turn to for financial education on fraud prevention and managing debt, 68.3% of respondents named their primary bank or credit union, followed by nonprofits like AARP (35%), federal agencies (34%), and state or local government (30%). For adults 60–74, that trust climbs to 72%. These are long-term customers with deep institutional relationships, and that trust creates a meaningful foundation for delivering fraud protection and financial education.

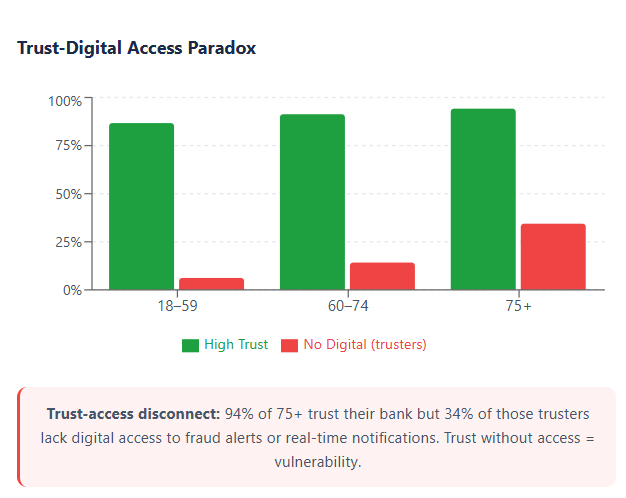

Trust and digital access by age

94% of adults 75 and older trust their primary bank — the highest rate of any age group. At the same time, 34% of adults 75+ have no digital access: no mobile app, no web login. For this group, real-time fraud alerts and digital safeguards may not be reaching them through the channels their bank primarily uses.

Figure 2. Trust rate vs. zero digital access rate by age group.

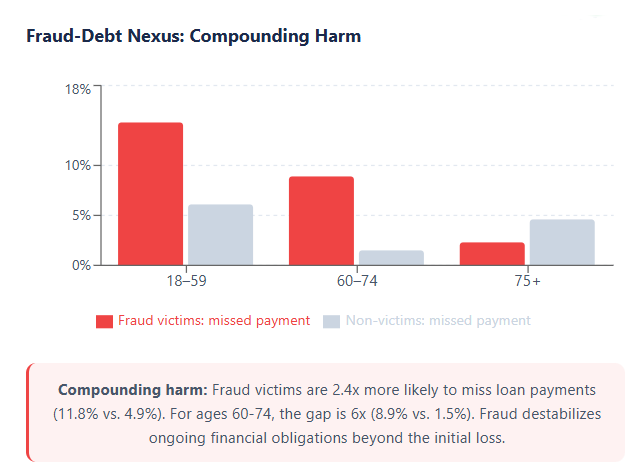

Compounding Harm: The Fraud-Debt Nexus

A stark gap in digital access is more than just a convenience issue; it is a critical vulnerability. When fraudulent activity goes unnoticed due to a lack of monitoring tools, the resulting damage multiplies. Fraud destabilizes ongoing financial obligations.

Figure 3. Compounding harm caused by financial fraud

Victims are 2.4 times more likely to miss loan payments compared to non-victims (11.8% vs. 4.9%). For adults aged 60-74, this gap becomes a six-fold increase (8.9% vs. 1.5%). These downstream effects—missed payments, damaged credit, and cascading fees—extend the harm far beyond the initial stolen amount. For an older adult on a fixed income, a single undetected scam can trigger a chain reaction that is incredibly difficult to recover from.

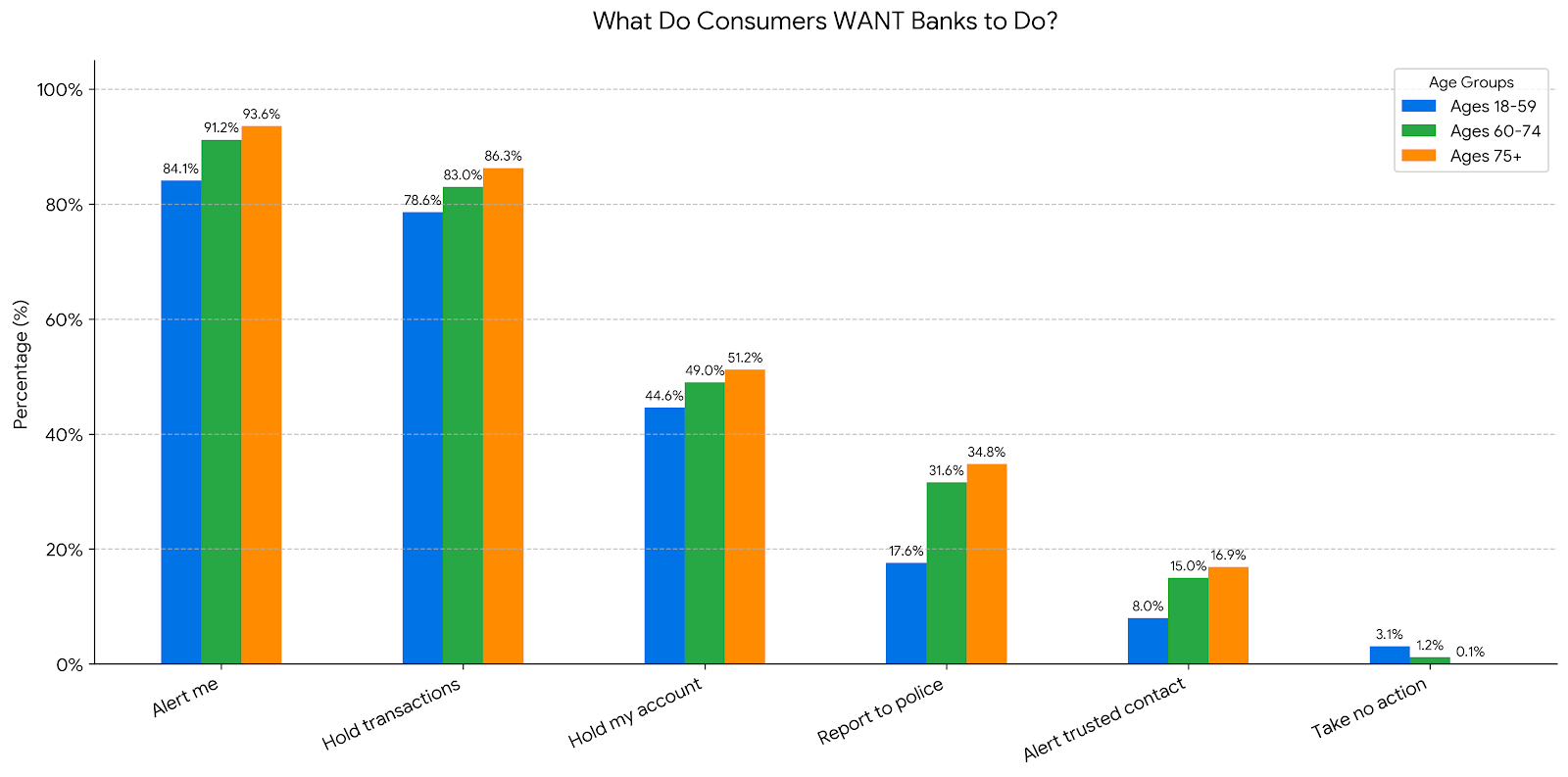

They Are Not Asking to Be Left Alone

While there might be a concern that proactive fraud interventions might feel paternalistic to older consumers, the data firmly contradicts this. The data firmly contradicts this. As the chart illustrates, rather than resenting bank involvement, the oldest consumers actually demand the highest levels of intervention. Across every protective measure, whether it is issuing direct alerts, holding suspicious transactions, or escalating to law enforcement, adults 75 and older consistently prefer more aggressive, proactive action from their banks than younger demographics. The desire for institutions to simply “take no action” is effectively zero.

Figure 4. Consumer protection expectations against fraud

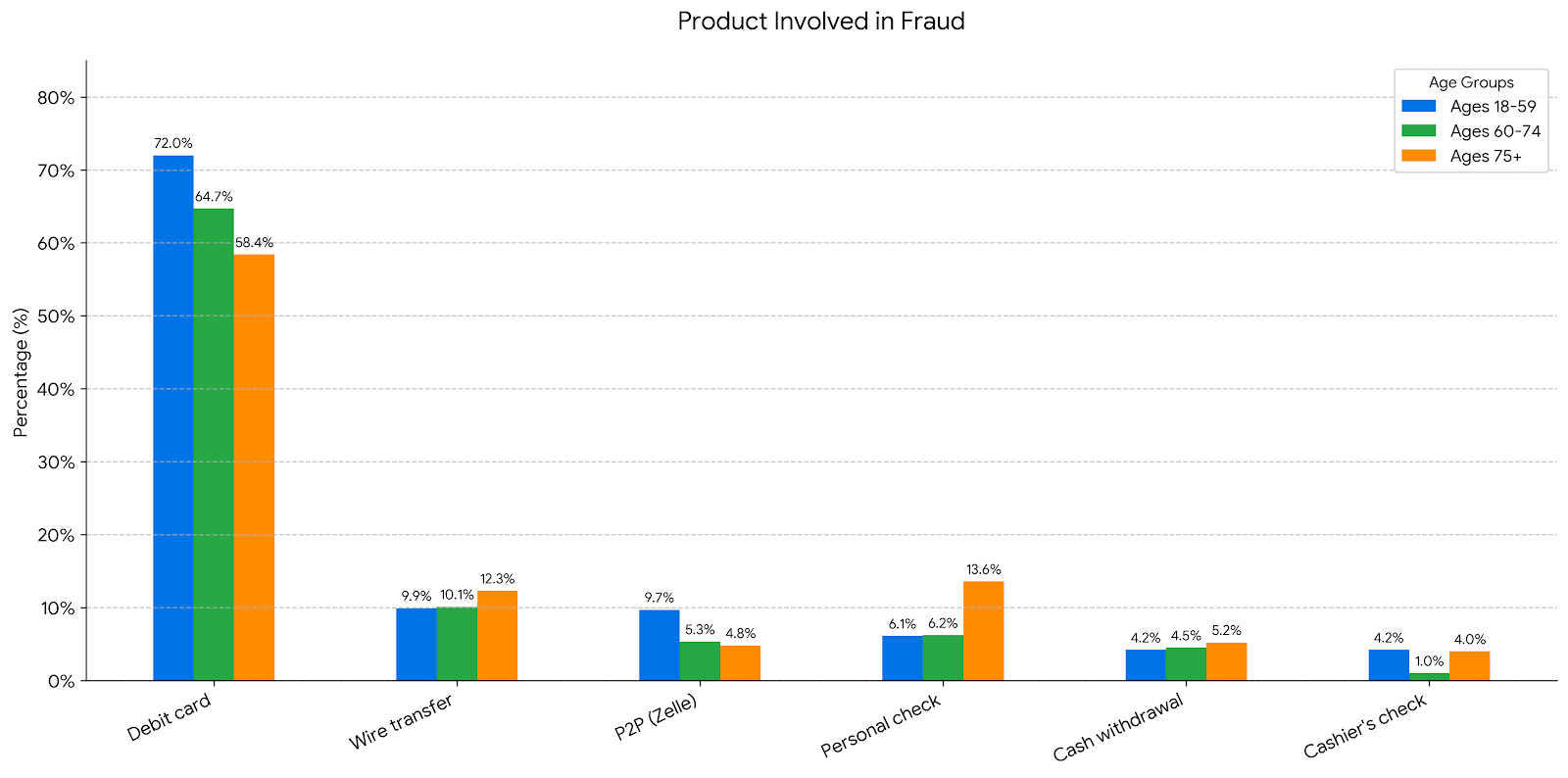

The Money Moves Through Old Infrastructure

Generational differences in banking products highlight where these vulnerabilities lie. While debit card usage dominates across all ages, it declines from 72% for younger adults to 58% for those 75+. Conversely, older adults rely more heavily on traditional, harder-to-reverse channels: personal check usage surges to 14%, and wire transfers climb to 12%. Meanwhile, P2P app usage (like Zelle) drops to 5%. Fraud tactics may be evolving, but the exploited infrastructure remains traditional.

Figure 5. Product fraud involvement by age group

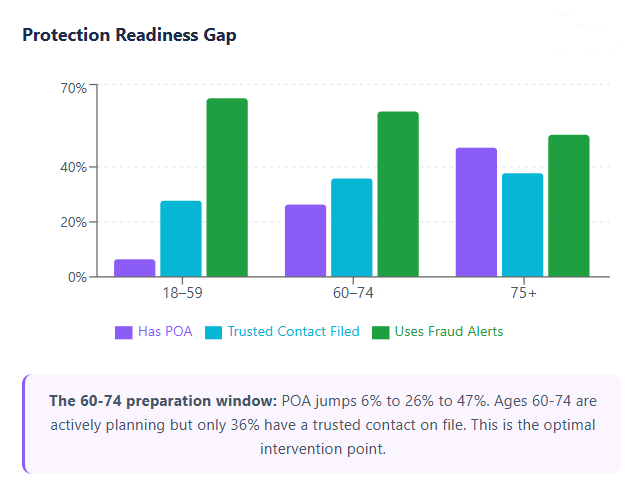

Ages 60-74: The Critical Intervention Window

Financial safeguarding behaviors shift dramatically around retirement age. Power of Attorney adoption quadruples from 6% (ages 18-59) to 26% (ages 60-74), eventually reaching 47% for those 75+. However, the rate of having a trusted contact on file plateaus after age 60, and active fraud alert usage actually declines. The 60-74 age band represents the optimal window for financial institutions and advocates to intervene and establish safeguards before habits set in and vulnerabilities compound.

Figure 6. Safeguard measures tracked across

What Both Datasets Tell Us

The complaint data I analyzed previously captured the severe end of the spectrum: high-dollar losses from people motivated enough to report. The NAFBS captures the broader picture, including the silent majority who experience fraud and never say anything. Together they point to the same conclusions:

Fraud is an everyone problem. Incidence is flat across age groups. The harm is not. The biggest risk often isn’t the initial loss — it’s what compounds afterward: missed payments, damaged credit, and a recovery that stretches far beyond the stolen amount. And older adults are not asking for less protection. Every data point in this survey says the opposite.

The Channel Gap is the Protection Gap

Ultimately, this data reveals a significant divergence between how security systems are designed and how consumers actually live. The industry has built sophisticated, mobile-first fraud alerts, often assuming older adults might resent the intervention. Instead, the numbers expose a stark Trust-Access Paradox: while 94% of adults over 75 deeply trust their primary institutions, 34% lack the digital access needed to actively monitor their accounts. They overwhelmingly want to be protected, but our default channels are missing them entirely.

The Power of Augmented Insight

Fraud prevention is a continuous evolving effort that requires us to adapt quickly without sacrificing precision. Uncovering structural vulnerabilities like the Trust-Access Paradox traditionally takes months of research. While the initial data release is accompanied by a foundational technical report, this personal weekend project demonstrates how AI can responsibly augment our analytical capabilities to rapidly surface actionable insights. By acting as a tool to rapidly parse and visualize complex datasets, AI helped surface these hidden gaps and identify the critical 60–74 “intervention window” in a fraction of the time. It proves that when applied thoughtfully, AI allows us to accelerate our understanding of raw survey data, turning it into actionable vulnerability maps to better protect consumers.

If the fraud epidemic is hidden in plain sight, this survey is one more flashlight.

***************

This analysis is just one piece of a broader effort to turn complex public datasets into actionable product strategy. You can interact with the full NAFBS dashboard along with my other AI-assisted visualizations of public fraud reports and consumer complaints at this new Interactive Data Hub.

Data source: CFPB National Age-Friendly Banking Survey Public Use File (n=2,721). Previous blog post: The Fraud Epidemic Hidden in Plain Sight

Disclaimer: Despite manual audits and triangulation across multiple models, AI-assisted analysis may still contain inaccuracies. The overarching patterns identified here are directionally reliable, but individual data points should be treated accordingly.