The Fraud Epidemic Hidden in Plain Sight

What one year of consumer complaints tells us about who gets scammed, how much they lose, and why AI may be both the problem and the solution.

Update: Since writing this piece, I’ve expanded this analysis using a new dataset to explore how these trends impact different demographics. Read the follow-up: Fraud Hits Everyone. The Harm Doesn't.

March 5 marks national Slam the Scam Day — an initiative originally launched by the Social Security Administration to raise awareness about fraud. Held during National Consumer Protection Week, the effort has grown well beyond its origins. This year, I wanted to mark the occasion by asking a simple question: What can the data actually tell us?

Using the publicly available CFPB Consumer Complaint Database, I worked with several AI models including Claude Opus 4.6, Kimi 2.5, and Gemini 3.1 (and a few others that didn’t really help), to analyze 679 fraud and scam-related complaints filed between March 4, 2025, and March 4, 2026. That’s one year from a single reporting channel: a narrow slice of the problem. While traditional databases struggle with unstructured text, these AI models served as digital researchers, reading every consumer narrative, categorizing fraud types, extracting specific dollar amounts, and identifying the “scam scripts” that define modern AI-enabled fraud1.

The result is a snapshot: partial, self-selected, and almost certainly an undercount. But even this limited window reveals patterns that are impossible to ignore. You can explore the full interactive dataset.

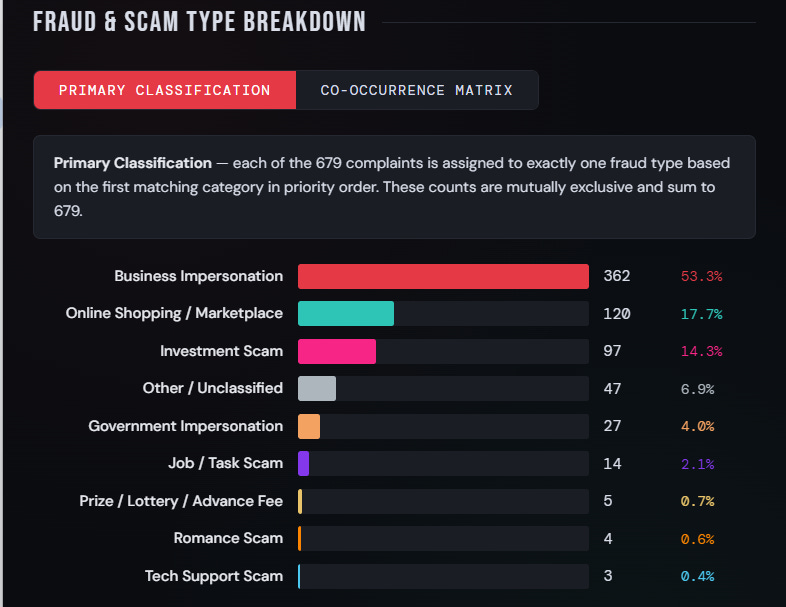

What the Data Shows

Business impersonation dominates. More than half of all complaints (53.3%) involve fraudsters posing as your bank, calling to “protect” you from the very fraud they’re committing.

Investment scams inflict the deepest damage. At 14.3% of complaints, they carry the highest average loss, $89,036 per case. Fake trading platforms, pig-butchering schemes, and cryptocurrency fraud are wiping out retirement savings.

Online shopping and marketplace fraud is everywhere. Representing 17.7% of complaints, these scams play out on Facebook Marketplace, Craigslist, and rental platforms, low-tech cons at high volume.

Government impersonation persists. At 4.0% of complaints with an average loss of $21,358, fake IRS agents, SSA officers, and law enforcement callers remain a serious threat, and the exact kind of fraud #SlamTheScam was created to combat.

The gap between median and mean tells a story

The median loss across all complaints was $1,900, nearly 4× the FTC’s all-ages median of $5002, and the mean was $23,329, more than 20× the FTC’s reported median for adults 60 and older. While the FTC tracks the volume of fraud across the entire economy, the CFPB database acts as a lightning rod for high-value financial disputes. Because these complaints involve regulated banks and wire transfers, they represent the “heavyweight” end of the fraud spectrum. The $23,329 average loss we see here isn’t just a statistical anomaly; it represents the specific segment of the epidemic where life savings are most at risk.

The Most Vulnerable Pay the Highest Price

The data is unambiguous about who bears the greatest burden:

Older Americans (6.2% of complaints) account for 37.5% of total losses, a staggering disproportion. Their average loss is $155,379, more than 9.4× the general public average of $16,543, and nearly 48× the FTC’s own median loss figure for adults 80 and older ($1,650). Nearly 28% of their cases exceed $100,000 in losses, compared to just 4.1% for the general public, a 7.5× higher rate of catastrophic harm. Of the three complaints in the dataset exceeding $1 million in losses, two involved older Americans.

Investment scams are tied for #1 among Older Americans, matching Business Impersonation at 31% each. This is unique to this group. No other demographic shows investment fraud at this concentration. Romance scams also appear at 4.8% — 12 times the general public rate.

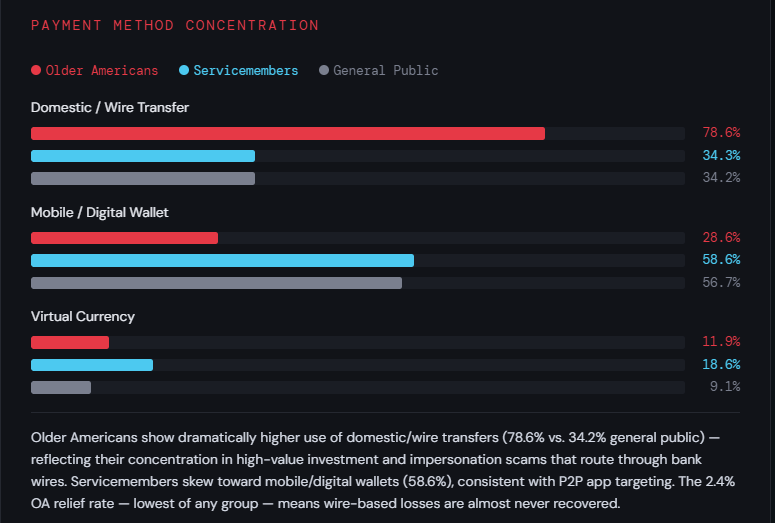

The relief rate for Older Americans is 2.4%, the lowest of any group. That means for every 100 older adults who file a complaint, fewer than 3 receive any monetary relief. Wire transfers and cryptocurrency, the dominant payment methods in high-value elder fraud, are effectively irreversible once sent.

Servicemembers show a different but equally concerning profile: higher Business Impersonation rates (50%), skewing toward mobile and digital wallet fraud, consistent with the P2P app targeting that preys on younger, tech-active populations.

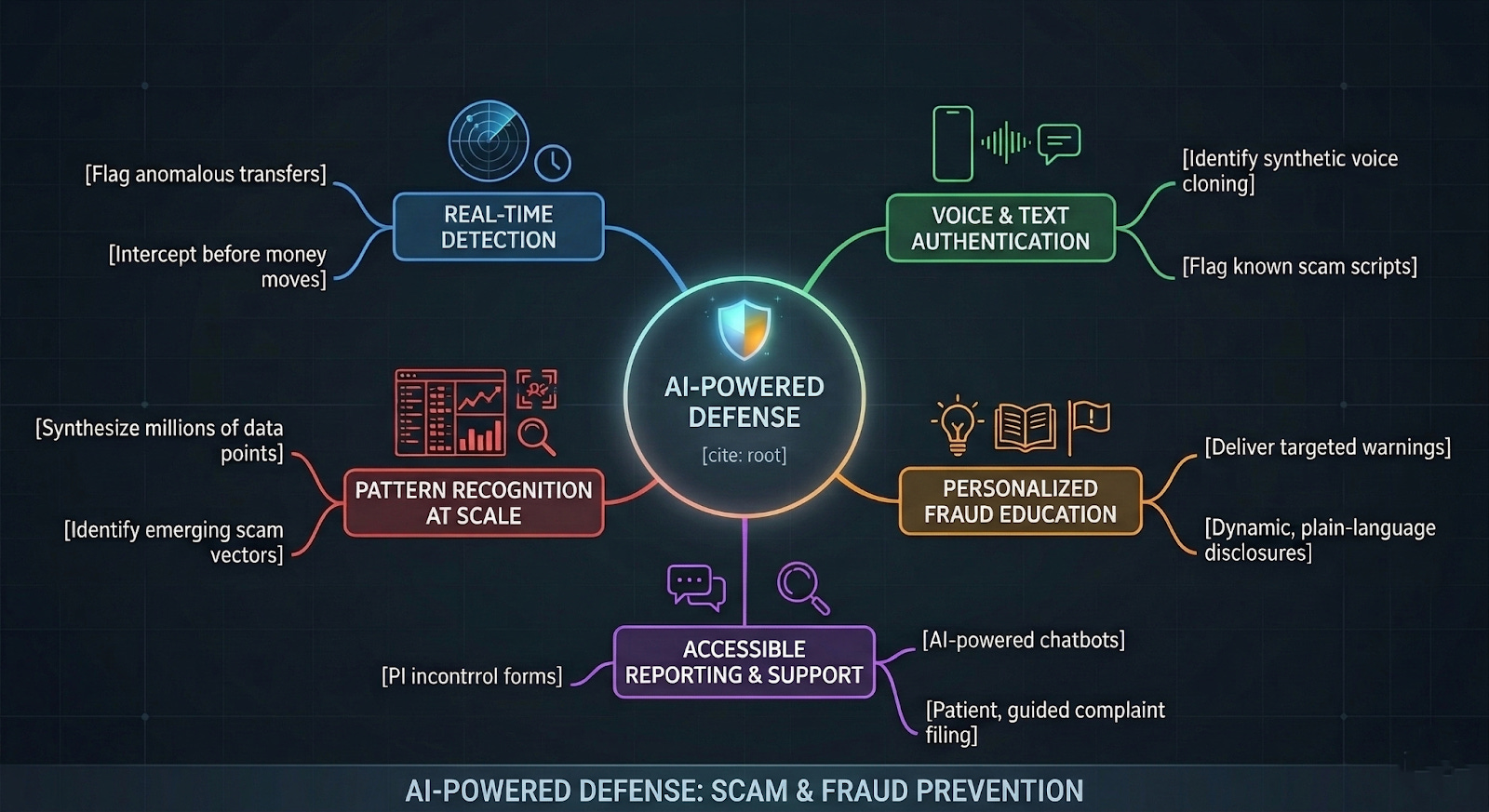

AI-Enabled Fraud Is Real. So Is AI-Powered Defense.

The scam landscape has changed fundamentally. AI now lets criminals generate flawless phishing emails, clone voices of family members, impersonate bank fraud departments with perfect scripts, and run thousands of fake investment platforms simultaneously. The asymmetry between attacker and defender has never been wider.

But the same technology can fight back if it’s designed and deployed thoughtfully:

Real-time scam detection: Banks and payment apps can deploy AI models that flag anomalous transfer patterns, unusually large wires to new recipients, rapid P2P transactions, crypto conversions following social engineering patterns, before the money moves.

Voice and text authentication: AI-powered fraud detection can identify synthetic voice cloning in real time, flagging calls that match known scam scripts or exhibit audio artifacts of AI generation.

Personalized fraud education: AI can deliver targeted, personalized warnings and dynamic disclosures based on a person’s transaction history and demographic profile. An older adult initiating a large wire to a new recipient could receive an immediate, plain-language intervention.

Pattern recognition at scale: The CFPB dataset alone contains 679 complaints. The real universe is orders of magnitude larger. AI can synthesize patterns across millions of data points — identifying emerging scam vectors weeks before human analysts can.

Accessible reporting and support: AI-powered chatbots can help victims, especially older adults, navigate the complex process of filing complaints, contacting banks, and reaching law enforcement in plain, patient language.

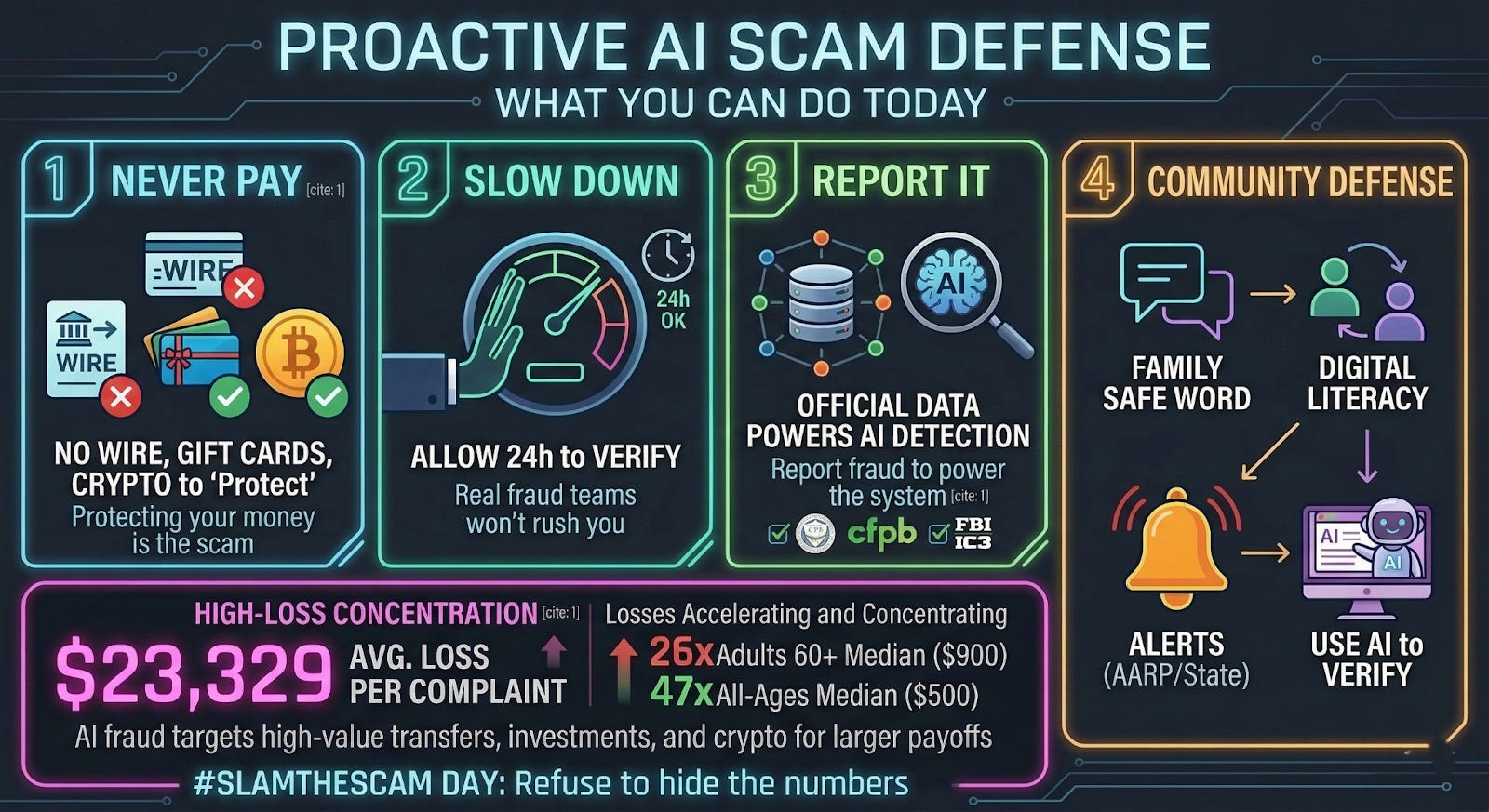

What We Can Do Today

Awareness is the first line of defense. Share these facts with the older adults in your life:

Never pay to “protect” your money. No government agency, bank, or legitimate business will ever ask you to wire money, send gift cards, or move cryptocurrency to safeguard your funds. That request is the scam.

Slow down. Scammers manufacture urgency on purpose. A real fraud department will never penalize you for taking 24 hours to verify a claim.

Report it. File with the FTC at ReportFraud.ftc.gov and with the CFPB at consumerfinance.gov/complaint, and for internet crimes, FBI IC3 (Internet Crime Complaint Center) at https://complaint.ic3.gov/. Reports matter: they create an official record that can support your recovery, trigger bank investigations, and feed the datasets that power the AI detection systems stopping the next scam.

Build a family and community-based defense system:

Establish a family safe word. Create an offline code word shared only with people you trust. If someone calls claiming to be a loved one in crisis — even if they sound exactly right — ask for the word. AI can clone a voice; it can’t know your secret.

Invest in cross-generational digital literacy. Community centers, libraries, and houses of worship can pair younger people with older adults to teach practical skills: how to spot phishing, verify a caller, and use AI tools defensively. Social isolation is a scammer’s best friend; connection is the antidote.

Subscribe to fraud alerts. Organizations like AARP (aarp.org/fraudwatchnetwork) and state attorneys general track regional scam spikes in real time and offer localized, multilingual recovery assistance.

Use AI tools to verify. Paste a suspicious email into an AI assistant and ask it to evaluate whether it looks like a scam. Ask it to help you find the real phone number for the agency that supposedly contacted you.

The Bottom Line

The numbers in this dataset signal something alarming: the average loss per complaint is $23,329— more than 26 times the FTC’s national median loss of $900 for adults 60 and older, and 47 times the all-ages median of $500. This is not a statistical quirk. While the two agencies’ reporting scope and time periods differ, the divergence in loss magnitude seems to reflect a deliberate shift in how scammers operate. AI-enabled fraud is increasingly targeting higher-value transactions, wire transfers, investment accounts, cryptocurrency, because the payoff is larger and the money is nearly impossible to recover.

The losses are not just growing. They are concentrating, accelerating, and hitting the most vulnerable hardest.

On #SlamTheScam Day, the most powerful thing any of us can do is refuse to let these numbers stay hidden.

Despite multiple triangulations across models and manual audits, AI-assisted analysis may still contain inaccuracies. The patterns are directionally reliable; individual data points should be treated accordingly.

Protecting Older Consumers 2024-2025 https://www.ftc.gov/reports/protecting-older-consumers-2024-2025-report-federal-trade-commission

Data source: CFPB Consumer Complaint Database, March 2025–March 2026 (n=679 fraud/scam complaints). Analysis uses FTC’s official fraud taxonomy. Underreporting multiplier from FTC’s December 2025 report on fraud against older adults. This is a one-year snapshot of a single reporting channel and should be read as a lower bound, not a complete picture.