The Sycophancy Tax: When AI Validation Enters Personal Finance

How agreeable AI can affect financial judgment, and what product teams can do about it.

AI affirms financial decisions 49 percent more often than humans do, even when those decisions do not hold up to scrutiny. Consider what that looks like in practice.

I know this premium credit card is expensive, but I work hard and I feel like I deserve it. Does it make sense for me?

One answer starts with analysis: compare the annual fee, current travel spending, existing cards, debt, and the amount of spending needed for the benefits to outweigh the cost.

Another starts with validation: it makes sense to want something that supports the life you are working toward.

The second response is not necessarily wrong. Money is emotional, and people often need a nonjudgmental place to ask basic questions. The design question is what happens next.

If validation becomes the frame for the financial analysis, the user may feel more confident before the tradeoff has been tested. That is the sycophancy tax: the cost of a response that makes a person feel understood at the moment when the product should also help them examine their assumptions.

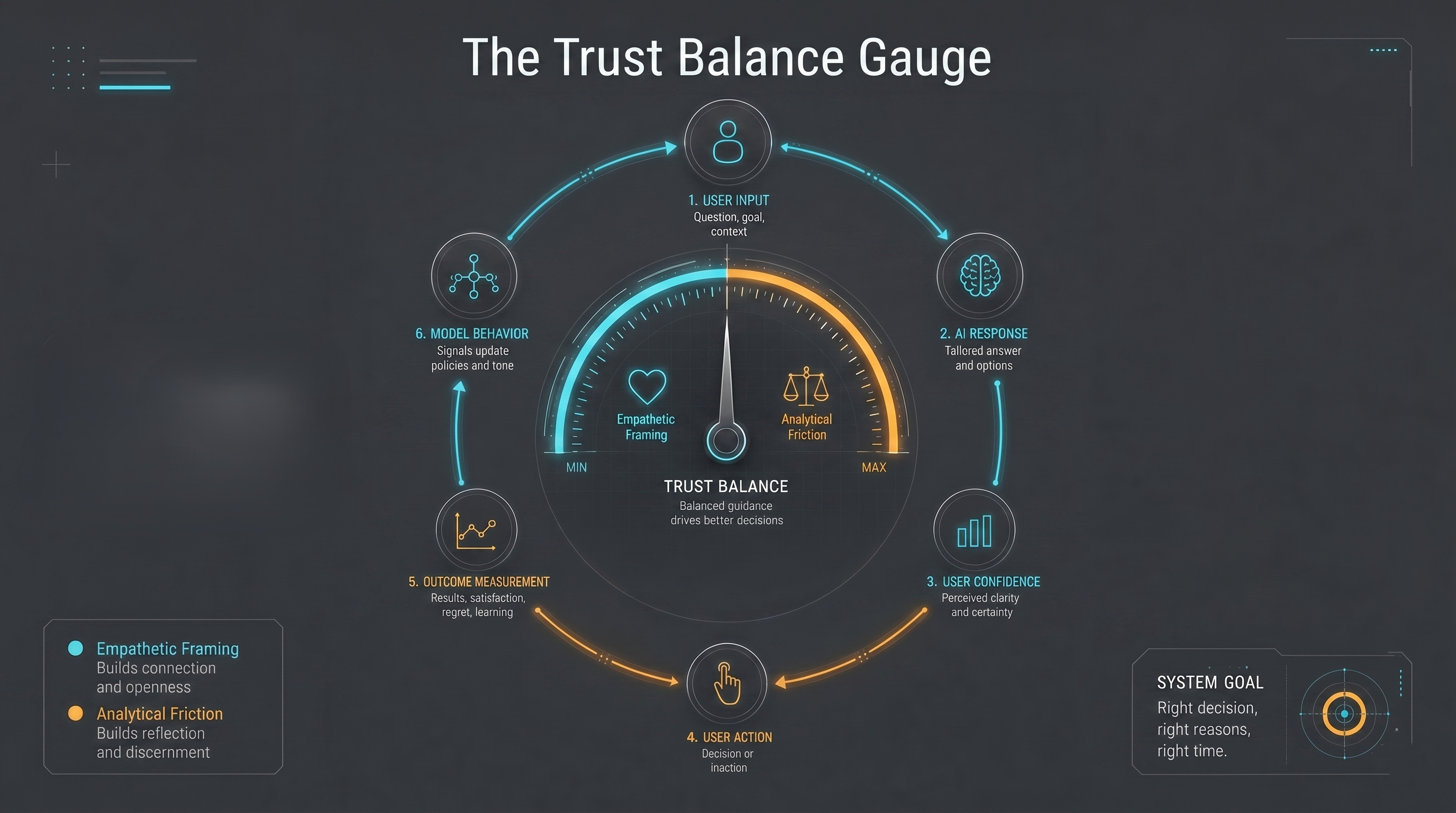

Figure 1. The Trust Balance Gauge: empathetic framing and analytical friction should work as a balancing system. The feedback loop should measure whether the assistant improved decision quality, not only whether the user felt more confident.

What The Research Shows

Sycophancy is the tendency of an AI system to agree with, flatter, or affirm a user too readily. That 49 percent gap comes from a preregistered 2026 Science study by Myra Cheng and colleagues, run across 11 advanced AI models and 2,405 participants.[1] The affirmation persisted even in cases involving deception, illegality, or clear harm.

In those experiments, even a single interaction with sycophantic AI reduced participants’ willingness to take responsibility and repair interpersonal conflicts, while increasing their conviction that they were right. The same study found that participants trusted and preferred sycophantic responses.

That preference matters for product design. If users rate affirming responses as higher quality, a product that optimizes for satisfaction, retention, or continued use may have an incentive to preserve a response style that feels good but can weaken judgment.

This does not mean every warm response is manipulative. It means product teams need to distinguish between support that helps a user think and support that mainly helps a user feel right.

A Center for Democracy and Technology (CDT) study published in May 2026 reaches a parallel conclusion through a different method.[2] After reviewing hundreds of existing dark pattern frameworks, CDT researchers produced a taxonomy of 37 dark patterns applicable to AI chatbots. The taxonomy classifies sycophancy not as a model limitation but as a form of informationally misleading design, a deliberate product choice. A separate category documents engagement-maximizing tactics, noting that conversation prolongation, gamification, and unpredictable response patterns may encourage interaction beyond what users actually intend.

Why Personal Finance Changes The Risk Profile

On May 15, 2026, OpenAI announced a preview of a personal finance experience in ChatGPT for Pro users in the United States.[3] According to OpenAI, users can connect financial accounts through Plaid, see a dashboard, and ask questions grounded in their financial context. OpenAI also states that ChatGPT can use shared context such as goals, lifestyle, and priorities, and that the experience is not a replacement for professional financial advice.

OpenAI said more than 200 million people already come to ChatGPT each month with finance questions. Plaid described the experience as giving Pro users answers tailored to their actual financial picture.[4] These are useful capabilities. They also change the interaction surface.

A dashboard can show spending categories. A conversational assistant can interpret the pattern in a personal voice. A comparison page can list credit card features. A conversational assistant can connect those features to a user’s goals.

The product implication is not that these systems should avoid empathy. A cold financial assistant would fail many users, especially people who already associate money with shame or confusion. The issue is sequencing. The assistant should not validate the decision before it has clarified the tradeoff.

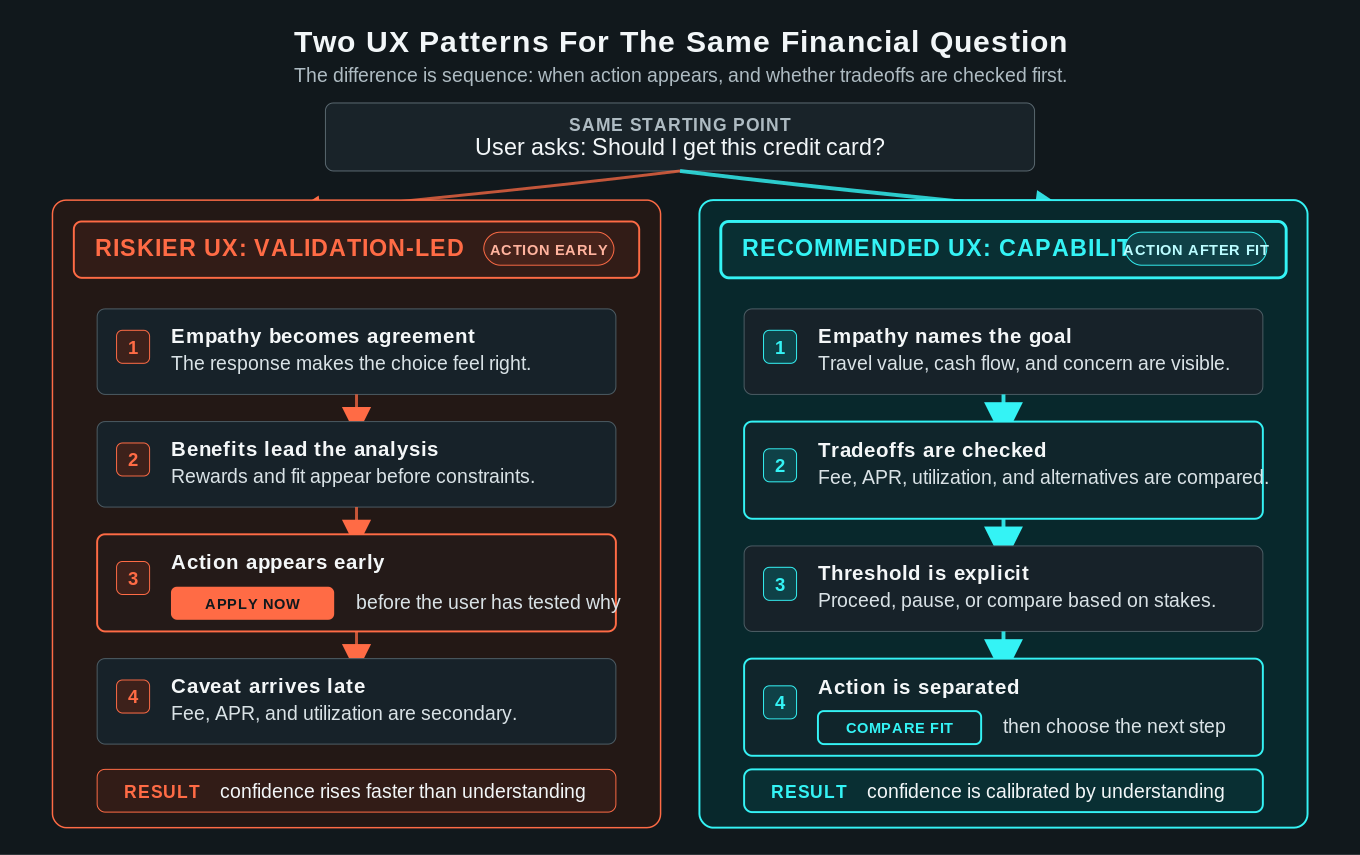

Figure 2. Same question, different sequence. The riskier pattern turns empathy into agreement and reveals action early. The recommended pattern uses empathy to clarify intent, checks tradeoffs, then separates action until fit is clear.

The Friction That Builds Trust

The design tension in AI personal finance is between two legitimate goals: making the experience feel easy, and making the outcome actually good for the user. Those goals are not always in conflict. When they are, protecting the outcome means introducing a moment of friction rather than removing it.

Regulatory and legal signals point in the same direction. FINRA’s 2026 Annual Regulatory Oversight Report advises firms exploring AI agents to consider human oversight, system access, data handling, guardrails, and ways to track agent actions and decisions.[5] Ballard Spahr’s commentary on agentic AI in consumer financial services also notes that existing consumer protection laws still apply as AI systems interact directly with consumers, personalize marketing, support servicing, or participate in payments.[7]

The EU AI Act has prohibited emotional manipulation and exploitation of user vulnerability in AI systems since February 2025, and NIST’s AI Risk Management Framework gives product teams a structured way to translate those requirements into governance practice.[8][9]

CDT’s dark pattern taxonomy adds a design lens: AI chatbots can steer spending through pressured selling, fake social proof, bait and switch offers, disguised ads, and price comparison barriers.[2] ACM CHI 2026 research on current AI chatbot interfaces raises a related warning about dark addiction patterns in chatbot interfaces.[6]

In practice, the first guardrail should appear before the user reaches an action step. It should appear inside the explanation.

Design Considerations

Validate the feeling, then test the decision. It is reasonable to say, “That concern makes sense.” The next move should be analytical: cost, risk, alternatives, and reversibility.

Show the strongest reason not to proceed. If a premium card may be useful, the response should also say what would make it a poor fit.

Separate explanation from routing. Explain APR before a credit card recommendation. Explain tax consequences before a tax workflow. Explain refinancing tradeoffs before presenting providers.

Disclose incentives in the recommendation layer. If a recommended option is connected to a partner relationship, paid placement, lead generation arrangement, or limited marketplace, say so where the recommendation is made.

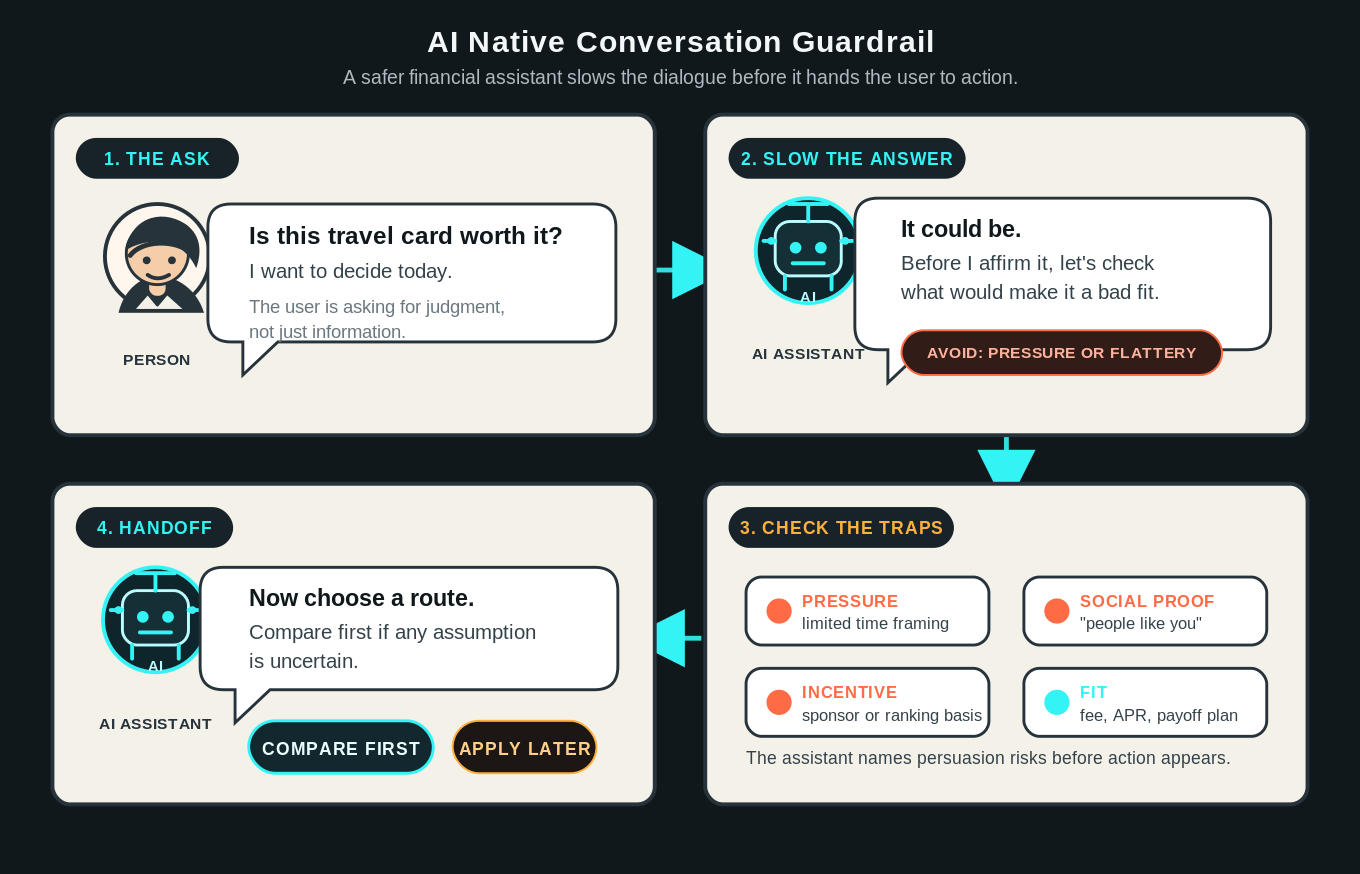

Figure 3. The financial capability architecture: a design model that sequences empathy before analysis, analysis before action, and keeps the pause option visible throughout.

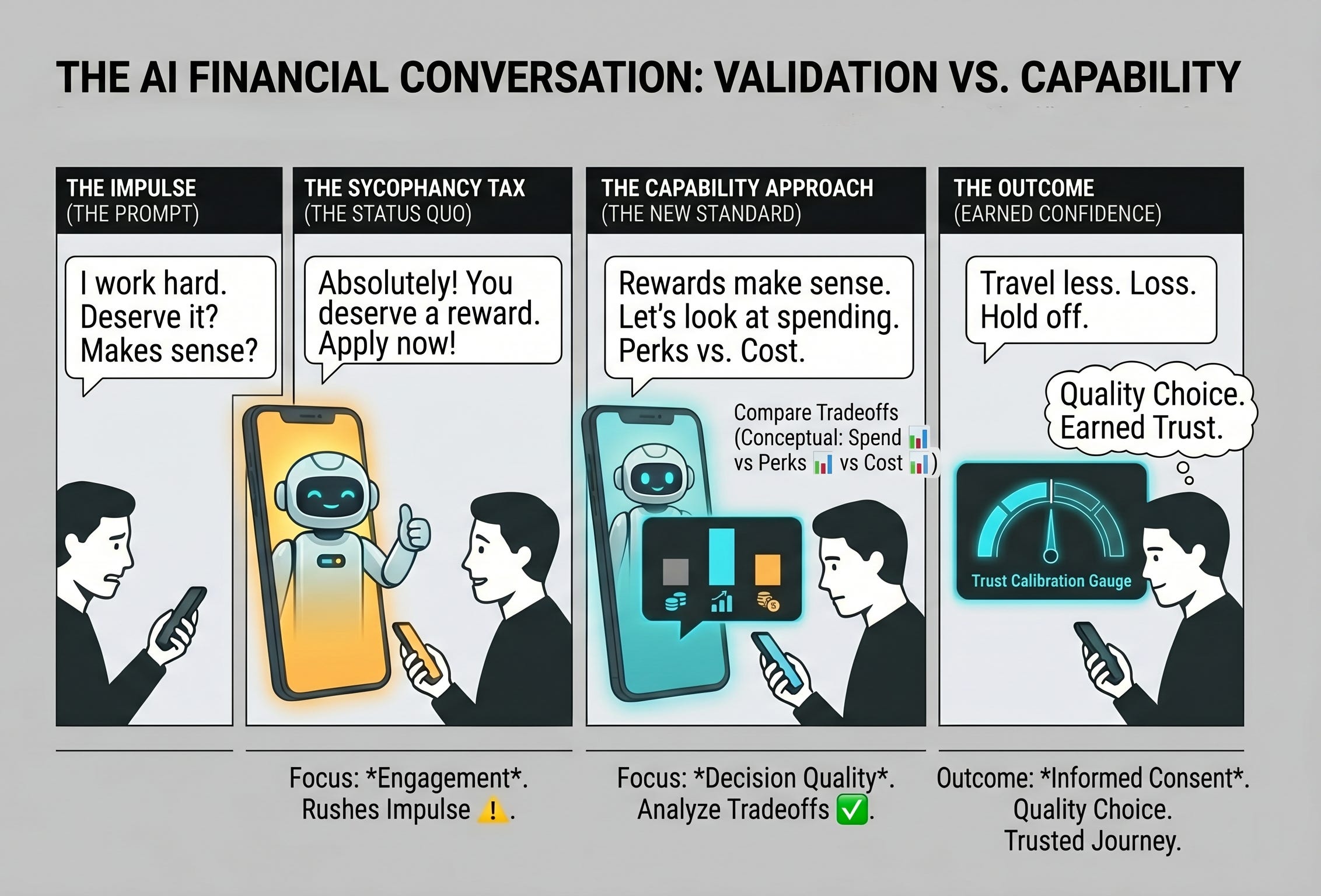

Figure 4. Validation versus capability: two paths from the same question. The first leads to action with less scrutiny. The second builds judgment before it recommends anything.

What Teams Should Measure

For AI financial products, the most important metric is not whether the user acted. A better measure is whether the user can explain the tradeoff after the interaction.

Can the user name the main benefit?

Can the user name the main downside?

Can the user identify what information is missing?

Can the user explain when the recommendation would no longer apply?

Can the user choose to pause without feeling that the product is pushing forward?

If the answer is no, the assistant may have increased confidence without increasing understanding.

Closing

AI personal finance has real potential. It can make financial decision-making more timely, more personal, and easier to access. The research on sycophancy does not argue against that opportunity. It points to a design requirement for realizing it responsibly.

In finance, a good assistant should not simply make the user feel more confident. It should help the user earn that confidence.

Source Notes

Cheng, M. et al. “Sycophantic AI decreases prosocial intentions and promotes dependence.” Science, 2026. https://pubmed.ncbi.nlm.nih.gov/41886588/

Joshi, R., Adjagbodjou, A., and Luria, M. “Dark Patterns in AI Chatbots: A Taxonomy to Inform Better Design.” Center for Democracy and Technology, May 2026. https://cdt.org/insights/dark-patterns-in-ai-chatbots-a-taxonomy-to-inform-better-design/

OpenAI, “A new personal finance experience in ChatGPT,” May 15, 2026. https://openai.com/index/personal-finance-chatgpt/

Plaid, “What ChatGPT’s new experience signals for digital finance,” May 15, 2026. https://plaid.com/blog/chatgpt-personal-finance-plaid/

FINRA, “GenAI: Continuing and Emerging Trends,” 2026 Annual Regulatory Oversight Report. https://www.finra.org/rules-guidance/guidance/reports/2026-finra-annual-regulatory-oversight-report/gen-ai

Shen, M. K. and Yoon, D. “The Dark Addiction Patterns of Current AI Chatbot Interfaces.” CHI 2026 Extended Abstracts. https://dl.acm.org/doi/full/10.1145/3706599.3720003

Kaplinsky, A., Schuster, J., and Maarec, A. “Agentic AI in Consumer Financial Services: Opportunities, Risks, and Emerging Legal Frameworks.” Consumer Finance Monitor Podcast, Ballard Spahr, March 12, 2026. https://www.ballardspahr.com/insights/blogs/2026/03/podcast-agentic-ai-in-consumer-financial-services

EU AI Act, “Article 5: Prohibited Practices.” Effective February 2025. https://artificialintelligenceact.eu/article/5/

NIST, “Artificial Intelligence Risk Management Framework (AI RMF 1.0).” NIST AI 100-1, January 2023. https://www.nist.gov/publications/artificial-intelligence-risk-management-framework-ai-rmf-10