We Can See $7.7 Billion of It. The Real Number May Be $81 Billion.

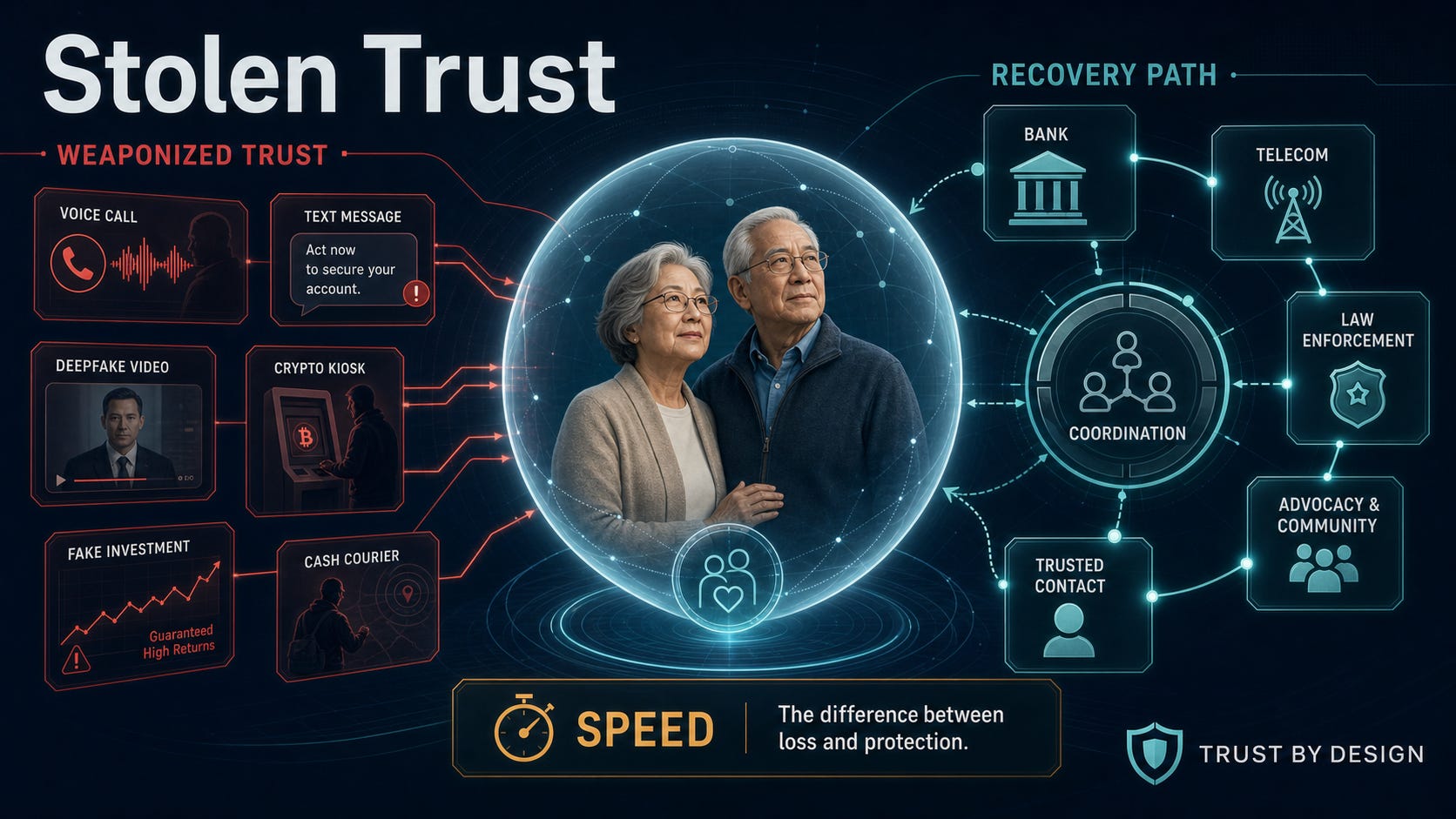

Elder fraud is now a coordinated industry. Our defenses still ask victims to find the right door while the money moves in minutes.

On June 15, 2026, the twentieth World Elder Abuse Awareness Day arrived with a harder truth than awareness campaigns usually carry. Twenty years ago the concern was often local: a bad actor, a stolen checkbook, a vulnerable person isolated from help. Today the data describes something closer to an industry: professionalized, transnational, and increasingly automated.

In my last two posts I traced who loses most and why. The CFPB complaint data showed older Americans, just 6.2% of complainants, carried 37.5% of the losses. The national banking survey then complicated the easy story: fraud incidence is roughly flat across age groups, but the harm is not, and older adults overwhelmingly want their banks to intervene.

A June 2026 study, Stolen Trust, by the nonprofit HCSK pulls the federal datasets into one picture [1]. Read alongside my earlier work, it points to a conclusion I did not expect: the central failure in elder fraud is no longer detection alone. It is response design. The money moves in minutes, the response takes days, the front door is a maze, and the safety advice still fights a threat that has already changed shape.

The gap is not only between fraud and awareness. It is between the speed of the theft and the design of the response.

The number we can see

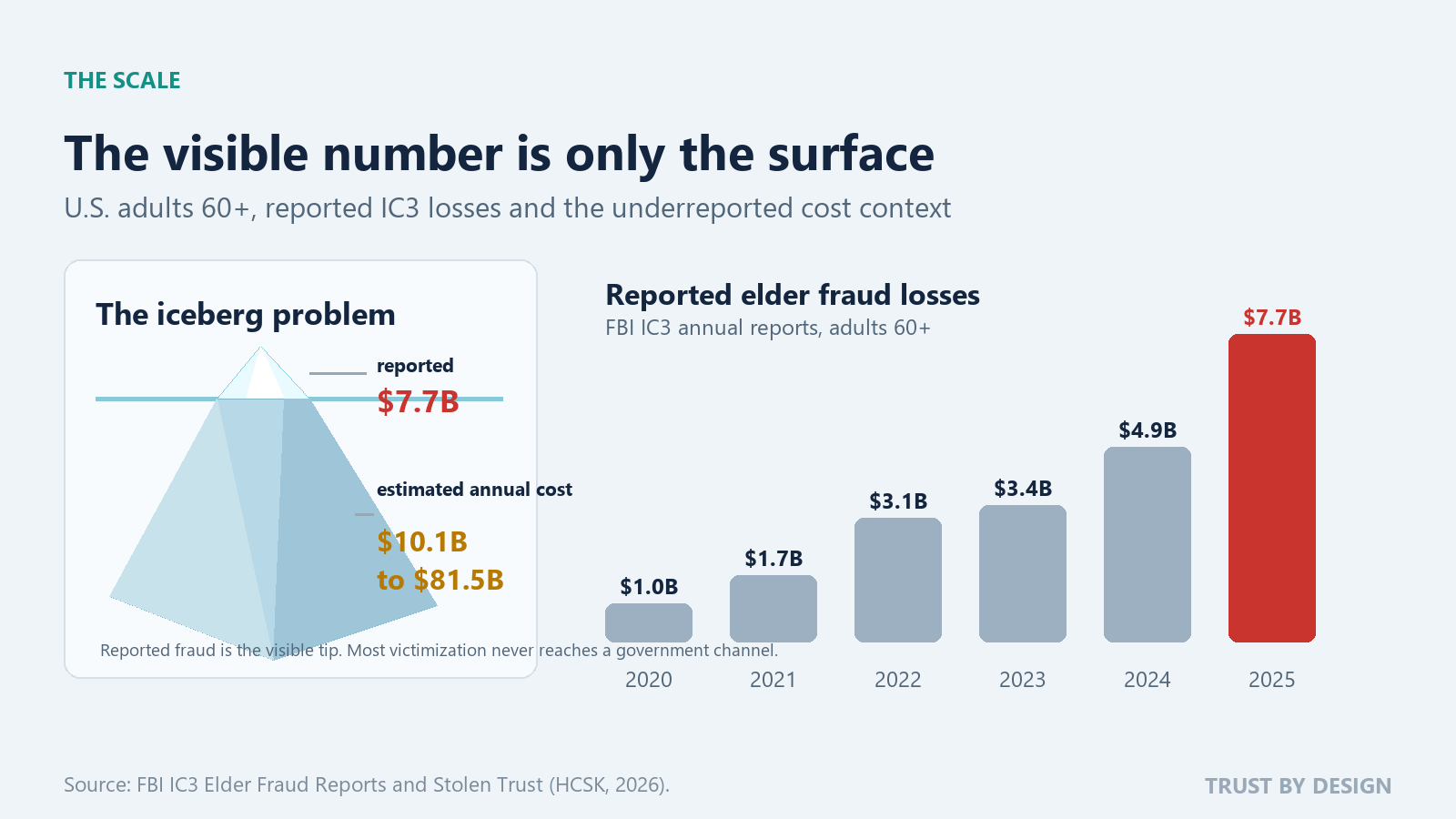

Reported elder fraud losses reached $7.7 billion in 2025 for U.S. adults 60 and over, across 201,266 complaints to the FBI's Internet Crime Complaint Center [1][2]. That is up 59% in a single year and roughly 360% since 2021. Adults 60 and over filed about 20% of all complaints but absorbed about 37% of all dollars lost.

Figure 1. The reported number is already large. The estimated true cost is much larger.

And the reported figure is only the visible tip. Using FTC underreporting estimates, Stolen Trust places the true cost to older adults somewhere between $10.1 billion and $81.5 billion a year [1][3]. The number we count is not the full problem. The number we cannot see is.

This is an industry now, not a con

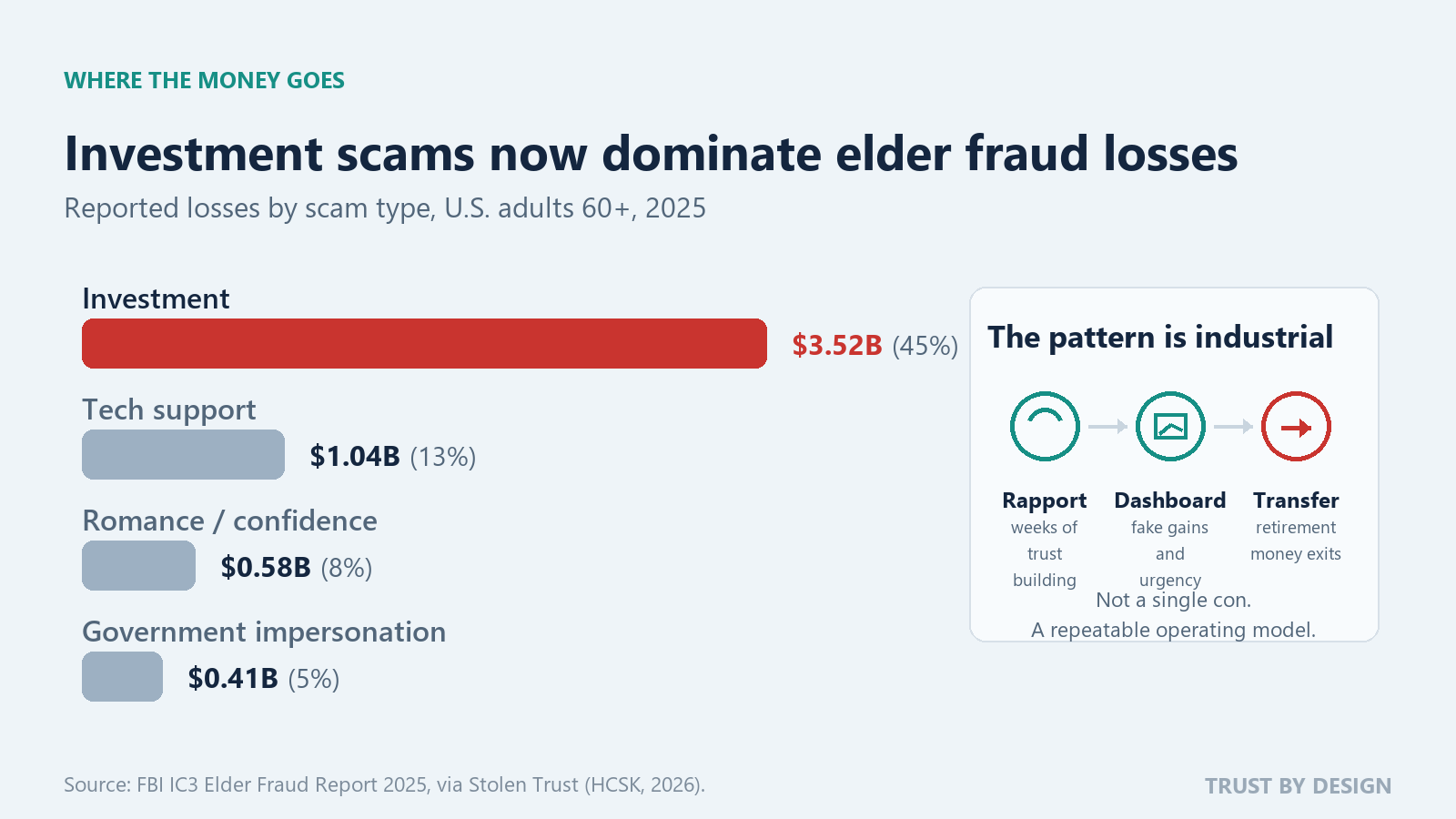

The composition of the losses tells the story of professionalization. Investment scams have grown roughly fifteenfold in five years and now account for 45% of all elder fraud losses, $3.519 billion in 2025, up 92% in a single year, with an average loss near $208,000 per victim [1][2]. Most follow the "pig butchering" pattern: weeks of warmth and rapport on social media or a dating app, a casual introduction to a "private" crypto platform with a convincing dashboard, small wins, then escalation until the victim liquidates retirement accounts and home equity, and finally the demand for "taxes" or "unlock fees" that signals the money is already gone.

Figure 2. Four scam types drive most elder fraud losses; investment fraud dominates.

The tooling behind these scams is now cheap, rented, and automated. A usable voice clone can be built from a 3-second audio clip lifted from a social media video. Deepfake video has put fabricated celebrity, and even fabricated doctor, endorsements behind fake investments. In June 2026, Google sued a China-based "smishing-as-a-service" operation that allegedly used generative AI to help scale text-message fraud, with subscriptions sold to other criminals for as little as $88 a week [6]. The crime then exits the digital world through stubbornly physical rails: the FBI logged 6,188 elder complaints about cryptocurrency kiosks in 2025, totaling $257.5 million, with older adults accounting for two-thirds of all kiosk losses across every age group [1]. The advice to "watch for bad grammar" was built for a threat that no longer exists.

This is the digital weaponization of trust. The scam no longer has to look sloppy to be dangerous. It has to look familiar, urgent, and just plausible enough to move someone from doubt to action before a second channel can intervene.

Seniors are not the weak link

It is tempting to read these numbers as evidence that older adults are easy marks. The data says the opposite. In the national figures, 74% of fraud reports filed by people 60 and over involved no monetary loss at all, meaning they recognized the scam and reported it anyway, and adults 60 and over were 62% more likely than younger adults to file such a no-loss report [1][3]. Experience is a real shield.

The danger is what happens when that shield breaks. The same group that spots most attempts suffers catastrophic losses on the few that succeed: the median loss for victims 80 and over is around $1,650, and a single investment scam averages more than $200,000 [1]. This is the bimodal reality behind the fraud-debt nexus I described earlier. The deepest damage is rarely the initial theft. It is the missed payments, the liquidated retirement, and a recovery that, on a fixed income, may never come.

The real failure is speed, not awareness

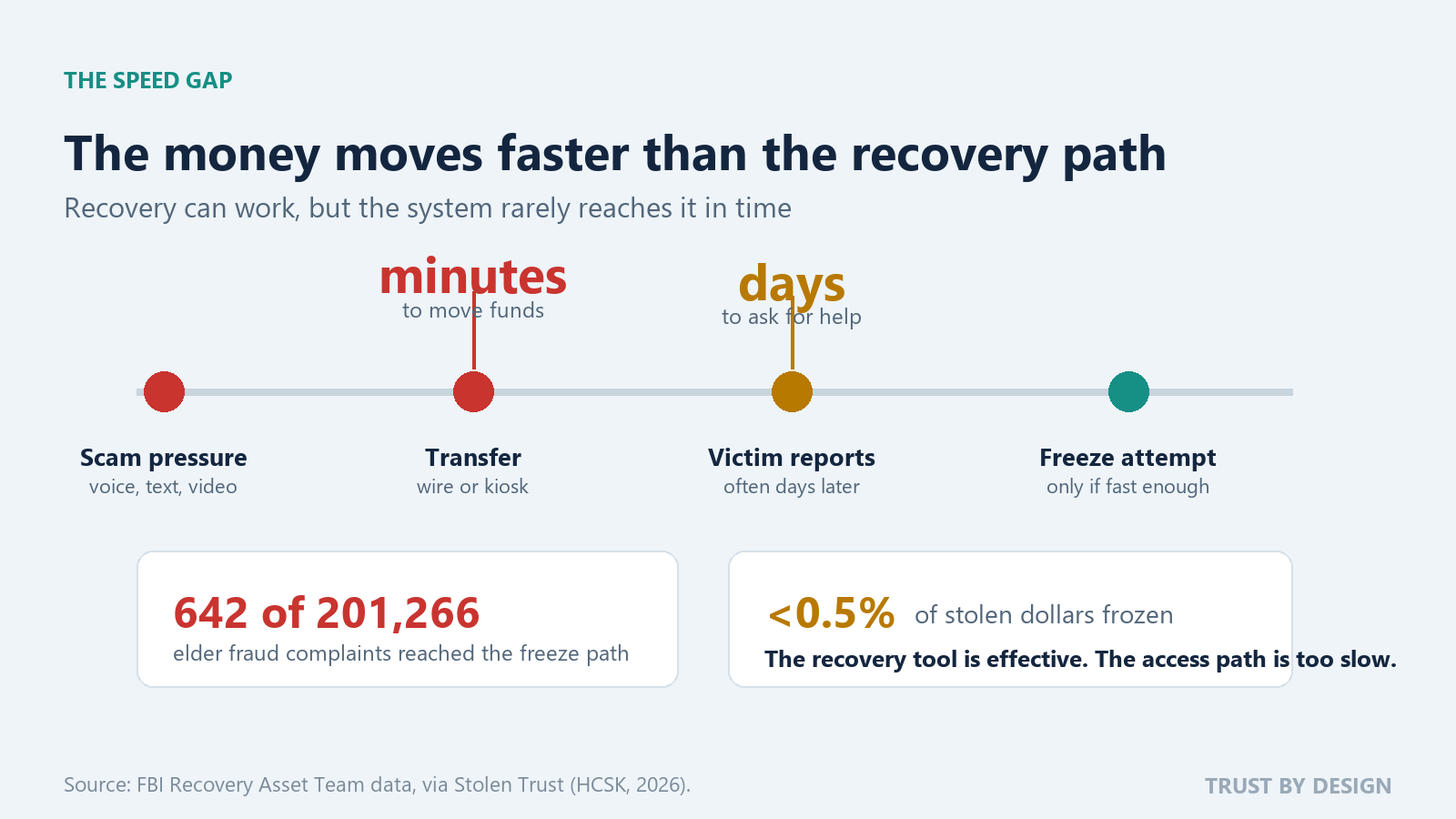

Here is the statistic that turns this from an awareness problem into a design problem. The FBI's Recovery Asset Team can freeze a fraudulent transfer, and when it reaches a case in time it freezes about half the money at risk. But in 2025 it reached only 642 of the 201,266 elder fraud complaints fast enough to act, and the total frozen came to less than half of one percent of the dollars stolen [1].

Figure 3. Recovery can work, but the current path rarely reaches it before the money moves.

The mismatch is structural. A crypto-kiosk transfer clears in minutes; a victim, often ashamed, may take days to report. Recent threat assessments covering April to June 2026 find the window to drain a victim has compressed from weeks to under 30 minutes in the worst observed cases, even as federal enforcement reached record levels, restraining nearly $800 million and disrupting more than 1.4 million scam accounts in a single operation [6]. And blocking the transfer is not the finish line: once a bank declines a wire, scammers increasingly pivot to in-person cash couriers, a shift serious enough that the FBI issued a dedicated alert in June 2026 [6]. The problem is not enforcement effort alone. It is that enforcement and recovery still move slower than the money.

Beyond the dollar

The cost does not stop at the balance sheet. The study documents what the tables cannot: depression, anxiety, insomnia, and social withdrawal are commonly reported after victimization, and federal programs now route some cryptocurrency-investment-fraud victims to suicide-intervention support [1]. Isolation is both a cause and a consequence, which is why the Surgeon General's framing of loneliness as a public-health issue belongs in this conversation. Shame keeps victims silent, and silence protects the next scam. Treating elder fraud as only a financial problem misses most of the harm.

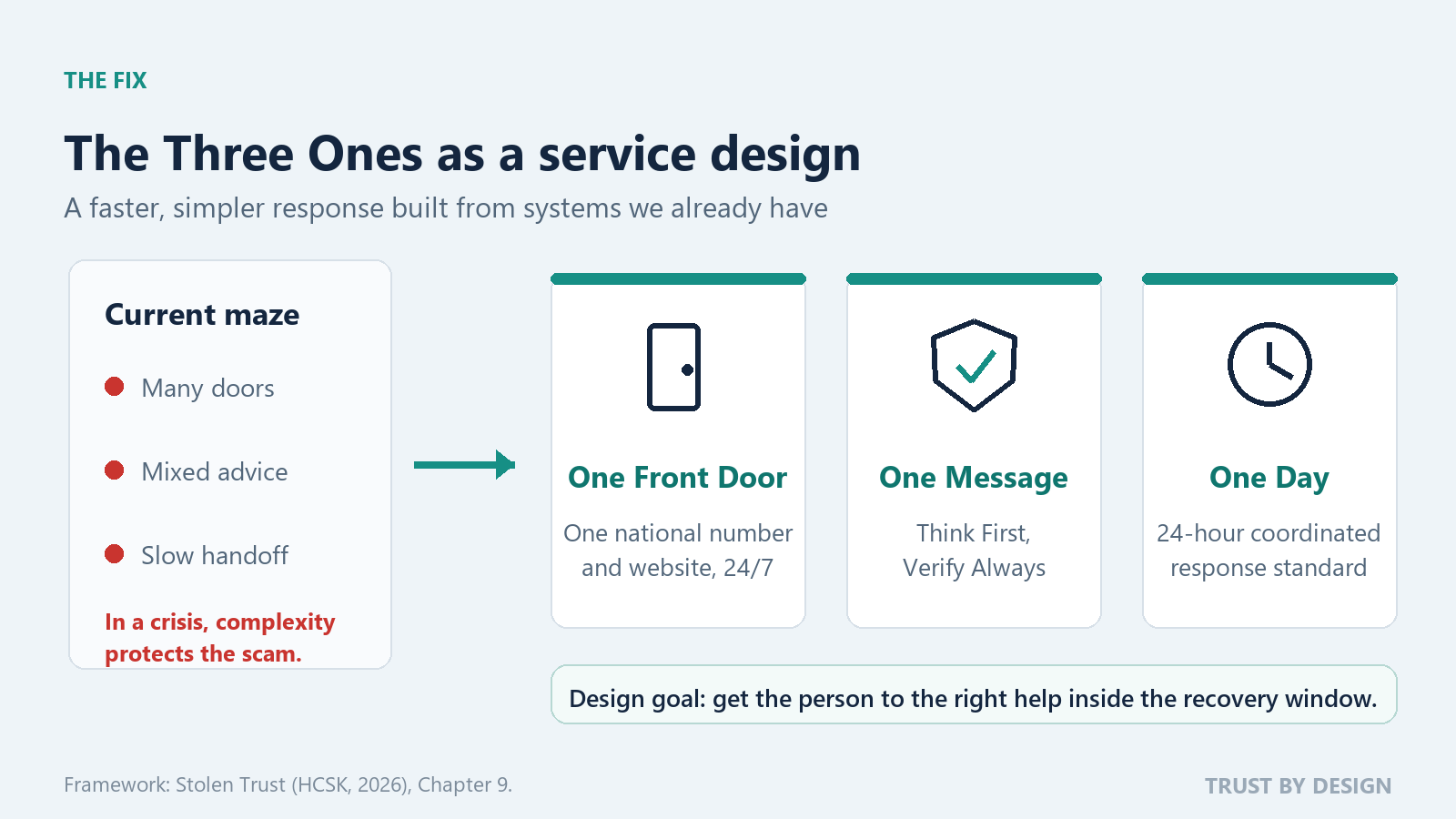

A design brief, not just a policy ask

Stolen Trust proposes a response it calls the Three Ones, built from infrastructure that mostly already exists [1]. It reads less like a policy memo than a service-design brief.

Figure 4. The Three Ones, read as a service-design response to three system failures.

One Front Door replaces a maze of hotlines and portals with a single number and website, so a frightened person reaches help inside the recovery window instead of giving up. One Message replaces cybersecurity jargon with a single behavioral rule, "Think First, Verify Always," aimed at manipulation rather than malware, and built on the premise that no inbound contact, by voice, video, or text, can be trusted on its face. One Day sets a 24-hour coordinated response standard, which only works with real data sharing between banks, telecom, and law enforcement, and defensive AI that can flag and hold an anomalous transfer before it clears.

What product and service teams can do now

Government agencies, banks, telecom providers, law enforcement, advocacy groups, and product teams are all working on pieces of the elder fraud response. The problem is not lack of effort. It is that the victim's path still crosses too many handoffs, too many channels, and too much delay. While policy coordination continues, product and service teams can make the recovery path faster, clearer, and easier to reach.

Build the front door into the product. Add a single, obvious "I think I have been scammed" path in the app and on the web, available 24/7. The user should not have to decide whether the right first step is a bank, a hotline, a police report, or a federal portal.

Intervene at the point of transfer. A plain-language "Think First, Verify Always" prompt on a large wire or first-time crypto-kiosk transaction embodies the One Message rule. The national survey showed older customers welcome that friction rather than resent it.

Treat a blocked transaction as the start of care. The courier pivot means the safest design adds a human follow-up after a declined transfer. Otherwise the scammer simply moves the victim to cash.

Design beyond the app. The Trust-Access Paradox still matters: 94% of adults over 75 trust their primary bank, yet about a third have no digital access. Protection has to travel through the phone and the branch, not only the screen.

And treat ages 60 to 74 as the intervention window: the moment to set up trusted contacts, alerts, and recovery preferences before habits and vulnerabilities harden.

The bottom line

Across three datasets now, the same conclusion keeps surfacing. Fraud is an everyone problem, but its harm is concentrated, accelerating, and falling hardest on people who often did everything right. So little money comes back not because victims failed to act, but because the system around them was never designed to act in time, in one place, against the threat actually being used.

We have the agencies, the laws, and the data. What we lack is coordination, simplicity, and speed, which are design problems before they are policy ones. Twenty years into elder fraud awareness, awareness is no longer the only gap. The fix is to stop asking people in crisis to navigate the maze and start building a faster door.

References

[1] HCSK. "Stolen Trust: A Special Study on America's Elder Fraud Landscape." June 2026. seniors.hcsk.org/special-study-2026

[2] FBI Internet Crime Complaint Center (IC3). "Elder Fraud Report 2025" and IC3 2025 Internet Crime Report.

[3] U.S. Federal Trade Commission. "Protecting Older Consumers 2024-2025: A Report of the Federal Trade Commission." December 2025.

[4] U.S. Department of Justice. "Elder Abuse Prevention and Prosecution Act (EAPPA) Report to Congress." 2025.

[5] Consumer Financial Protection Bureau. "Recovering from Elder Financial Exploitation." September 2022.

[6] Cyber News Network. "SENTINEL-FRAUD: U.S. Consumer Scam Threat Assessment." June 10, 2026 (window April 26 to June 10) and June 17, 2026. Source for the sub-30-minute loss window, enforcement restraint totals and 1.4M-account disruption, the FBI June 2026 cash-courier alert (I-061526-PSA), and the Google smishing-as-a-service lawsuit.